ST. PAUL, Minn., November 7, 2022 – Today, St. Paul-based AgriBank announced financial results for the third quarter of 2022, with strong profitability, credit quality, and liquidity and capital.

Highlights:

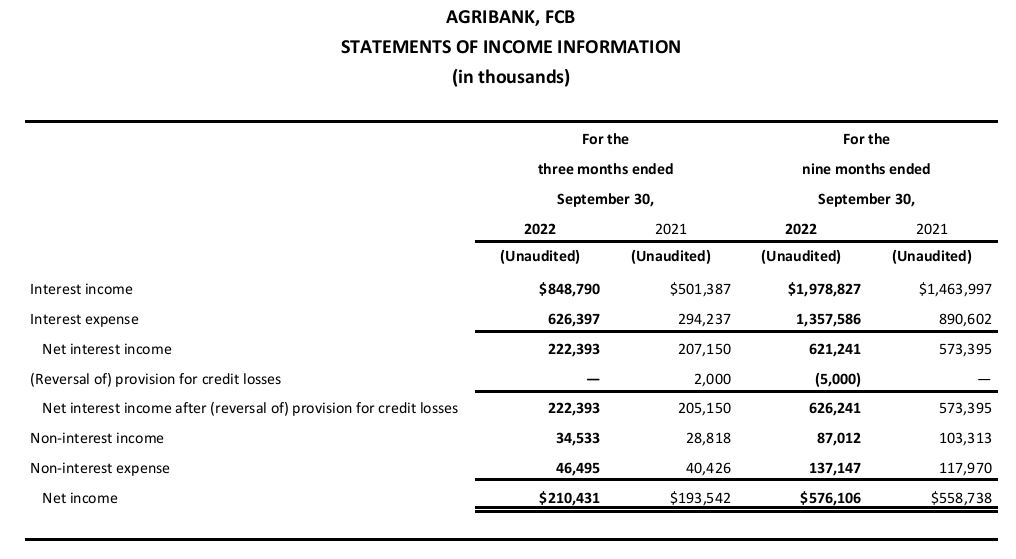

- Profitability: Net income remained strong at $576.1 million for the nine months ended September 30, 2022. AgriBank’s year-to-date return on assets (ROA) ratio of 53 basis points was above the target of 50 basis points.

- Credit quality: Total loan portfolio credit quality was strong, with 99.4 percent of loans classified as acceptable at September 30, 2022, compared to 98.3 percent at December 31, 2021.

- Liquidity and capital: End-of-the-quarter liquidity was 159 days, well above the regulatory requirement. Capital also remained well above the regulatory minimums and company targets.

“AgriBank recorded continued strong financial performance in the third quarter of 2022,” said Jeffrey Swanhorst, AgriBank chief executive officer. “Loan volume increased and credit quality improved, driving strong profitability. We are well positioned to support the Farm Credit lenders we fund as they work with their borrowers in navigating headwinds, including highly volatile agriculture product prices, continued operating cost inflation, increased interest rates, and the volatile global economic and political environment.”

Year-to-date 2022 Results of Operations

Net interest income was $621.2 million for the nine months ended September 30, 2022, an increase of $47.8 million, or 8.3 percent, compared to the same period of the prior year. Net interest income increased mainly due to increases within the crop input financing, asset pools and equipment financing portfolios.

Non-interest income was $87.0 million for the nine months ended September 30, 2022, a decrease of $16.3 million, or 15.8 percent, compared to the same period of the prior year. As interest rates have risen, loan prepayment and conversion activity has slowed, resulting in lower fee income. Partially offsetting these decreases, mineral income has increased due to higher oil prices.

Non-interest expense increased $19.2 million, or 16.3 percent, for the nine months ended September 30, 2022 compared to the same period of the prior year. The increase was primarily driven by an increase in loan servicing fees related to pool programs and higher Farm Credit System Insurance Corporation insurance premiums.

Loan Portfolio

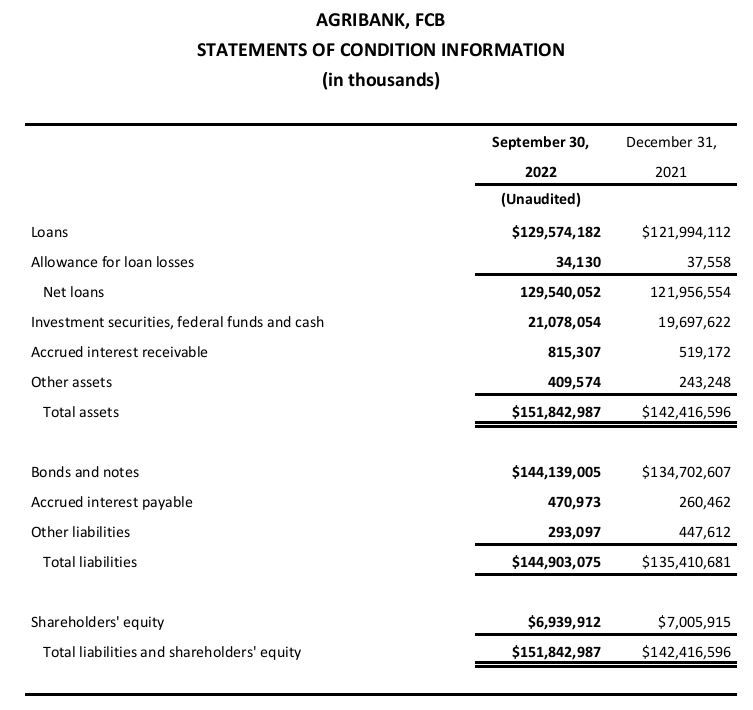

Total loans were $129.6 billion at September 30, 2022, an increase of $7.6 billion, or 6.2 percent, compared to December 31, 2021. This increase, mainly in AgriBank’s wholesale portfolio, was primarily driven by a rise in agribusiness and real estate mortgage volume throughout the AgriBank District, partially offset by declines in production and intermediate-term volume.

AgriBank’s credit quality reflects the overall financial strength of District Associations and their underlying portfolios of retail loans. AgriBank’s portfolio was composed of 99.4 percent loans classified as acceptable as of September 30, 2022, compared to 98.3 percent at December 31, 2021. Loans classified as acceptable represent the highest-quality assets. The credit quality of AgriBank’s retail loan portfolio decreased slightly to 95.2 percent classified as acceptable at September 30, 2022, compared to 95.4 percent acceptable at December 31, 2021.

Agricultural Conditions

The U.S. Department of Agriculture’s Economic Research Service (USDA-ERS) updated its 2022 forecast of the U.S. aggregate farm income and financial conditions on September 1, 2022. The release also converted the 2021 forecasts to estimates. The updated figures showed substantial upward revisions to farm sector income, equity and working capital for both 2021 and 2022 compared to the February 2022 projections. Estimated 2021 net farm income (NFI) was revised up by $21.3 billion from the February 2022 forecast to $140.4 billion. That is up $45.9 billion from 2020 in nominal terms and marks the second highest inflation-adjusted level since the mid-1970s. The upward revision to the 2021 estimate was due to a $20.3 billion downward revision in total expenses. USDA operator surveys showed lower than previously forecast intermediate product expenses, capital consumption, labor costs, and interest expenses for 2021, which were behind the lower overall expense estimate.

Despite all the challenges and uncertainty in markets the past few years, the U.S. agriculture sector is positioned well in 2022, and farm balance sheets are strong. Many factors, including weather, trade, government and monetary policy, global agricultural production levels, and pathogenic outbreaks in livestock and poultry, may keep agriculture market volatility elevated for the next few years. Implementation of cost-saving technologies, marketing methods and risk management strategies will continue to cause a wide range of results among the respective agricultural producers.

Capital Resources and Liquidity

Total capital remained very strong at $6.9 billion as of September 30, 2022, a decrease of $66.0 million compared to December 31, 2021. While net income and net stock issuances positively impacted shareholders’ equity, these increases were more than offset by unrealized investment losses, primarily on U.S. treasuries and U.S. government guaranteed mortgage-backed securities, related to the rapid increase in interest rates. AgriBank exceeded all regulatory capital minimum requirements, including additional regulatory buffers.

Cash and investments totaled $21.1 billion and $19.7 billion at September 30, 2022 and December 31, 2021, respectively. AgriBank’s end-of-the-period liquidity position represented 159 days coverage of maturing debt obligations, which supports operational demands, and was well above the 90-day minimum established by AgriBank’s regulator.

About AgriBank

AgriBank is part of the customer-owned, nationwide Farm Credit System. Under Farm Credit’s cooperative structure, AgriBank is primarily owned by local Farm Credit Associations, which provide financial products and services to rural communities and agriculture. AgriBank obtains funds and provides funding and financial solutions to those Associations. The AgriBank District covers a 15-state area stretching from Wyoming to Ohio and Minnesota to Arkansas. For more information, please visit www.AgriBank.com.

Forward-Looking Statements

Any forward-looking statements in this press release are based on current expectations and are subject to uncertainty and changes in circumstances. Actual results may differ materially from expectations due to a number of risks and uncertainties. More information about these risks and uncertainties is contained in AgriBank’s annual report, which is available no later than 75 days following the end of the year. AgriBank undertakes no duty to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.